On March 20, 2026, mortgage interest rates are making headlines, and for good reason. The mortgage interest rate—the cost of borrowing money from a lender to buy a home—has become a pivotal factor for homeowners and potential buyers alike. Whether you're looking to purchase a new home or refinance an existing mortgage, the current landscape is one of uncertainty and opportunity. This article dives into the latest trends, compares 30-year mortgage rates, and offers a critical look at what's driving the market in 2026.

Unraveling the Trends in 30-Year Mortgage Rates

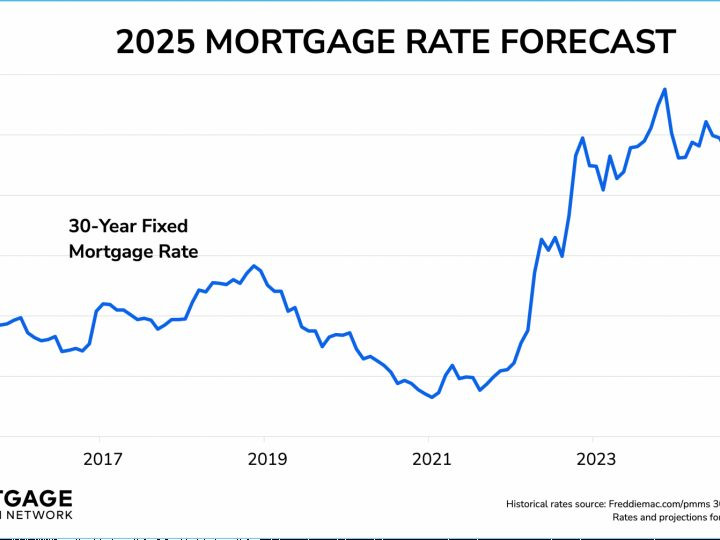

The 30-year mortgage rate remains the gold standard for mortgages, with roughly 90% of homeowners opting for this fixed-rate option. This has been a staple for decades, providing stability and predictability for borrowers. As of March 20, 2026, the average 30-year fixed-rate mortgage hovers around 6.25%, a figure that reflects a volatile economic climate and the Federal Reserve's ongoing efforts to combat inflation.

This increase in rates has led to a surge in demand for mortgage refinance rates, as homeowners look to lock in lower rates before they climb even higher. However, the data is damning: the rush to refinance has been met with a tight lending market, making it harder for some borrowers to secure favorable terms.

Let's not kid ourselves, the market is tough. The recent uptick in rates has put a damper on the housing market, slowing down both sales and refinancing. The average borrower is now paying more in interest, which can significantly impact monthly payments and long-term financial planning. The Federal Reserve's aggressive rate hikes are aimed at curbing inflation, but the collateral damage is real for homeowners.

Comparing Current Refinance Rates and Lenders

For those considering a mortgage refinance, the current landscape is a mixed bag. While rates are higher than they were a year ago, there are still opportunities to save money, especially for homeowners whose current rates are significantly higher. Comparisons show that refinancing can still be a smart move for those with older mortgages, but the window is narrowing.

The competition among mortgage lenders is fierce, with many offering incentives to attract borrowers. From lower origination fees to flexible repayment terms, lenders are pulling out all the stops to stay competitive. For potential borrowers, this means more options and potentially better deals, but it also requires careful research and comparison. Here’s what nobody’s asking: Are these deals sustainable, or are lenders simply trying to offset the market downturn?

Checking today's rates and comparing offers can help borrowers make informed decisions. Rates vary by lender and location, so it's crucial to shop around. For example, Accunet Mortgage provides easy-to-read charts that can help homeowners compare current rates and find the best deals.

Expert Insights: The Future of Mortgage Interest Rates

Experts predict that mortgage rates will continue to fluctuate in the coming months, influenced by economic indicators and Federal Reserve policies. Freddie Mac’s Primary Mortgage Market Survey (PMMS) has been a reliable indicator of market trends, showing a steady increase in rates over the past year.

As of now, the outlook is cautious. Refinancing rates may stabilize, but the overall trend suggests that homeowners should brace for a period of higher borrowing costs. Here’s the expert view: "The volatility in interest rates is a direct reflection of the broader economic uncertainty. Homeowners should be prepared for fluctuations and consider locking in rates if they find a favorable offer.

"We’ve seen a surge in demand for fixed-rate mortgages as borrowers seek stability amidst the economic turmoil. This trend is likely to continue as long as inflation remains a concern."