Let's not kid ourselves — today, March 27, 2026, is a pivotal day for homeowners. Mortgage refinance rates are at a crossroads, and savvy homeowners are eyeing the best deals to save thousands. With interest rates fluctuating, it's time to dive into the world of mortgage rates today and understand the nuances of 30-year mortgage rates and the impact of mortgage interest rates on your finances.

Understanding Today’s Refinance Rates: A Deep Dive

The mortgage landscape is a labyrinth of numbers, percentages, and acronyms. Today, March 27, 2026, it's crucial to grasp the nuances of refinance rates and how they can impact your financial health. According to Rocket Mortgage, refinance rates are a game-changer, allowing homeowners to pay their mortgage off faster or get cash out to fund other projects. But here’s what nobody’s asking: how do these rates stack up against historical trends, and are they really the best deal in town?

The Shape of Today’s Mortgage Rates: Trends and Predictions

With the current mortgage rates today in flux, it’s essential to stay informed. According to Chase, mortgage refinance interest rates are updated daily and backed by an experienced team of mortgage professionals. This dynamic environment means that rates can change overnight, making it vital to act quickly. When comparing 30-year mortgage rates, it’s clear that slight variations can add up to significant savings over time. However, it’s not just about the numbers — it’s about understanding the broader economic context and how it influences mortgage interest rates today.

Comparing Refinance Rates: Finding the Best Deal

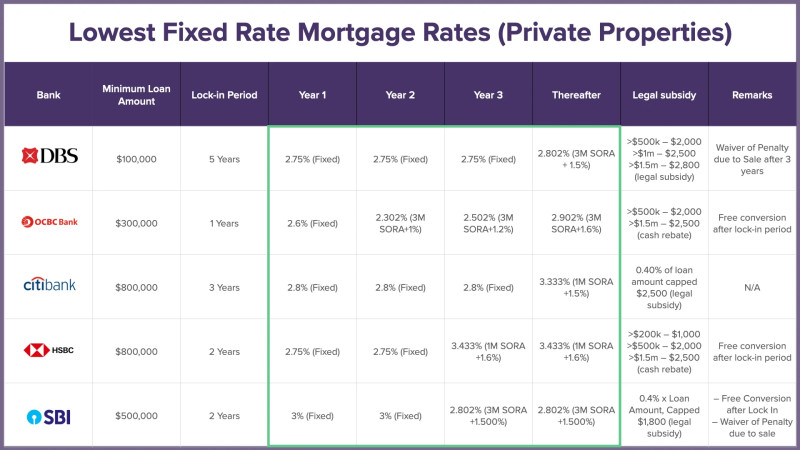

When it comes to comparing refinance rates today, there are a few key factors to consider. According to Forbes, comparing the average APR on 30- and 15-year fixed and 5/1 ARM refinances can help you make an informed decision. Similarly, U.S. Bank updates its refinancing rates daily, offering a range of loan options to suit different needs. The tables provided offer a clear breakdown, making it easier to compare today's mortgage rates based on your specific criteria. For example, if you are in the market for a 30-year mortgage, it's crucial to weigh the pros and cons of locking in a fixed rate versus an adjustable-rate mortgage (ARM).

Here’s a counterpoint: while many experts advocate for locking in a fixed rate, some argue that ARMs can provide flexibility, especially in a fluctuating market. However, the data is damning — fixed rates have historically offered more stability, making them a safer bet for long-term planning.

So, here’s what nobody’s asking: are you ready to seize the moment and make a move? With mortgage refinance rates at a critical juncture, the time to act is now. Whether you’re looking to lower your monthly payments, shorten your loan term, or tap into your home’s equity, today’s rates offer a unique opportunity. Don’t let this chance slip through your fingers — explore your options, compare rates, and take control of your financial future.

As you delve deeper, remember to check out Bankrate’s comprehensive comparison tool, which allows you to see how much you can save by refinancing your mortgage. Additionally, NerdWallet and Zillow offer valuable insights and tools to help you navigate the complex world of mortgage refinancing. The current mortgage rates today, as of March 27, 2026, are a golden opportunity to secure a better financial future.

Let’s face it, the mortgage interest rates are a lot like the weather—always changing, always unpredictable. But unlike the weather, mortgage refinance rates offer a chance to take control and make a significant impact on your financial health. So, are you ready to take the plunge and make the most of today’s rates? Don't let this opportunity slip away, and remember, the clock is ticking on these favorable rates.